Discover the 75/15/10 rule—a simple budgeting method to save 15% of your income, crush debt, and still enjoy life. Learn if it’s right for you!”

Are you overwhelmed by budgeting methods? From the 50/30/20 rule to zero-based budgeting, it’s easy to get lost in the noise. But what if there’s a simpler way to manage your money without spreadsheets or apps? Enter the 75/15/10 rule—a minimalist, percentage-based strategy that prioritizes essentials, savings, and guilt-free spending.

In this guide, you’ll learn:

- What the 75/15/10 rule is (and how it compares to other budgeting frameworks)

- Step-by-step instructions to implement it

- Who this method works best for (and who should avoid it)

- How to customize it for your unique financial goals

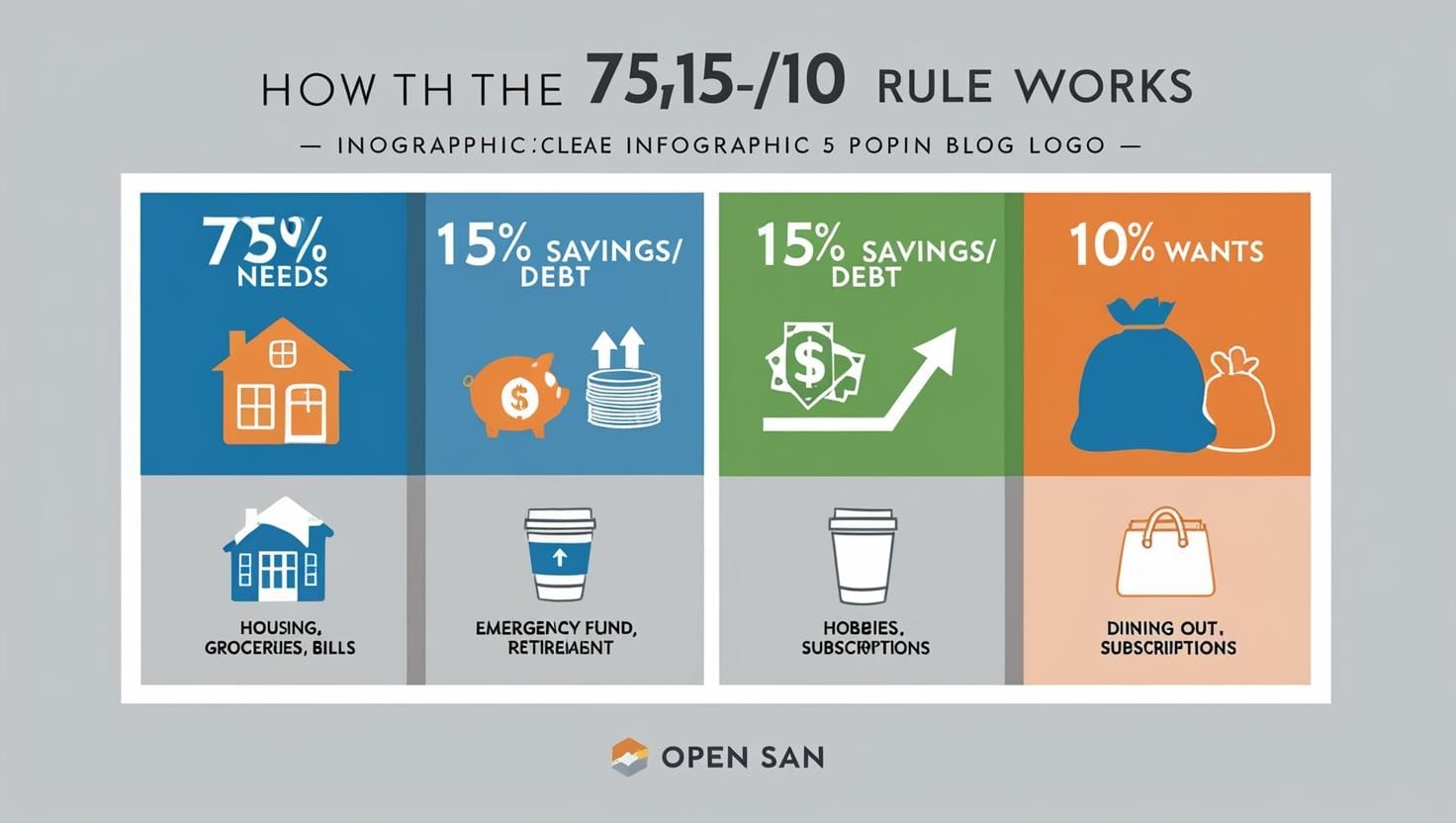

What Is the 75/15/10 Rule?

The 75/15/10 rule is a percentage-based budgeting system that divides your after-tax income into three categories:

- 75% for Needs: Essential expenses like housing, utilities, groceries, insurance, and minimum debt payments.

- 15% for Savings & Debt Repayment: Emergency funds, retirement accounts (e.g., 401(k)), and extra debt payments beyond the minimum.

- 10% for Wants: Non-essential spending like dining out, travel, hobbies, or subscriptions.

Unlike the popular 50/30/20 rule, the 75/15/10 method prioritizes aggressive saving and debt payoff while tightening spending on wants. It’s ideal for people who want to:

- Escape paycheck-to-paycheck cycles

- Pay off debt faster

- Build wealth without tracking every dollar

How the 75/15/10 Rule Works: A Real-Life Example

Let’s say your monthly take-home pay is $4,000:

| Category | Percentage | Amount | Examples |

|---|---|---|---|

| Needs | 75% | $3,000 | Rent, utilities, groceries, insurance, debt |

| Savings/Debt | 15% | $600 | Emergency fund, retirement, extra debt payments |

| Wants | 10% | $400 | Dining out, travel, hobbies, subscriptions |

Why it works: It creates clear boundaries, reduces decision fatigue, and forces you to prioritize long-term goals over lifestyle inflation.

Pros and Cons of the 75/15/10 Rule

Pros

Simplicity: No micromanaging categories—just three buckets.

Debt Focus: Allocates 15% to crushing debt or building savings.

Flexibility: Works for variable incomes (e.g., freelancers) if you adjust percentages monthly.

Cons

Rigid for High-Cost Areas: If housing eats 50% of your income (common in cities like NYC or SF), sticking to 75% for all needs is tough.

Limited “Fun Money”: 10% for wants may feel restrictive if you value experiences or hobbies.

Not for Low Incomes: If essentials exceed 75%, this method isn’t sustainable.

75/15/10 vs. Other Budgeting Methods

Here’s a quick comparison of popular budgeting frameworks:

| Budgeting Method | Needs | Wants | Savings/Debt | Best For |

|---|---|---|---|---|

| 75/15/10 Rule | 75% | 10% | 15% | Aggressive savers, debt repayment |

| 50/30/20 Rule | 50% | 30% | 20% | Balanced lifestyles, moderate savers |

| Zero-Based Budget | Variable | Variable | Variable | Detail-oriented planners |

| Pay-Yourself-First | Flexible | Flexible | Priority | Minimalists, irregular income earners |

Winner: The 75/15/10 rule shines for debt payoff and frugal spenders who want to automate savings.

How to Customize the 75/15/10 Rule for Your Goals

- Adjust Percentages:

- If you earn $6k/month but live in a high-cost area, try 80/10/10.

- If debt-free, shift the 15% to investments (e.g., 75/20/5).

- Use Hybrid Strategies:

- Pair it with the envelope system for cash-based spending on wants.

- Combine with sinking funds for irregular expenses (e.g., car repairs).

- Automate It:

- Direct deposit savings/debt payments to separate accounts.

- Use apps like Qapital or Digit to automate the 15% savings rule.

Who Should Use the 75/15/10 Rule?

- Debt Repayment Warriors: Perfect for paying off credit cards or student loans.

- Minimalists: If you hate tracking 20+ categories, this simplifies life.

- High Earners with Discipline: Those who can keep lifestyle inflation in check.

Avoid it if:

- Your essential expenses exceed 75% of income.

- You’re building a business or have irregular income.

Step-by-Step Guide to Start the 75/15/10 Budget

- Calculate After-Tax Income: Include salary, side hustles, and passive income.

- Categorize Essentials: List needs (rent, utilities, groceries, insurance).

- Trim Excess: If needs exceed 75%, cut costs (e.g., refinance debt, downsize housing).

- Automate Savings: Send 15% to savings/debt accounts on payday.

- Track Wants: Use a debit card or app to cap spending at 10%.

Pro Tip: Review every 3 months. Life changes—so should your budget!

FAQs

Q: Is the 75/15/10 rule better than the 50/30/20?

A: It depends! The 75/15/10 is better for aggressive savers, while 50/30/20 offers more flexibility for wants.

Q: What if my needs exceed 75% of my income?

A: Prioritize increasing income (side hustles, raises) or reduce fixed costs (cheaper housing, refinancing debt).

Q: Can I use the 75/15/10 rule with a variable income?

A: Yes! Calculate percentages based on your lowest monthly income to stay safe.

Conclusion: Is the 75/15/10 Rule Right for You?

The 75/15/10 rule isn’t a one-size-fits-all solution, but it’s a powerful tool for simplifying finances and accelerating savings. If you’re tired of complex budgets and want to focus on big wins (like debt freedom or retirement), give it a 3-month trial.

Ready to start? Share this post, bookmark it, and tag someone who needs a budget reset!

COMMENT WHICH BUDGETING METHOD DO YOU USE ?